#1 Finance Super App

based on average monthly active users

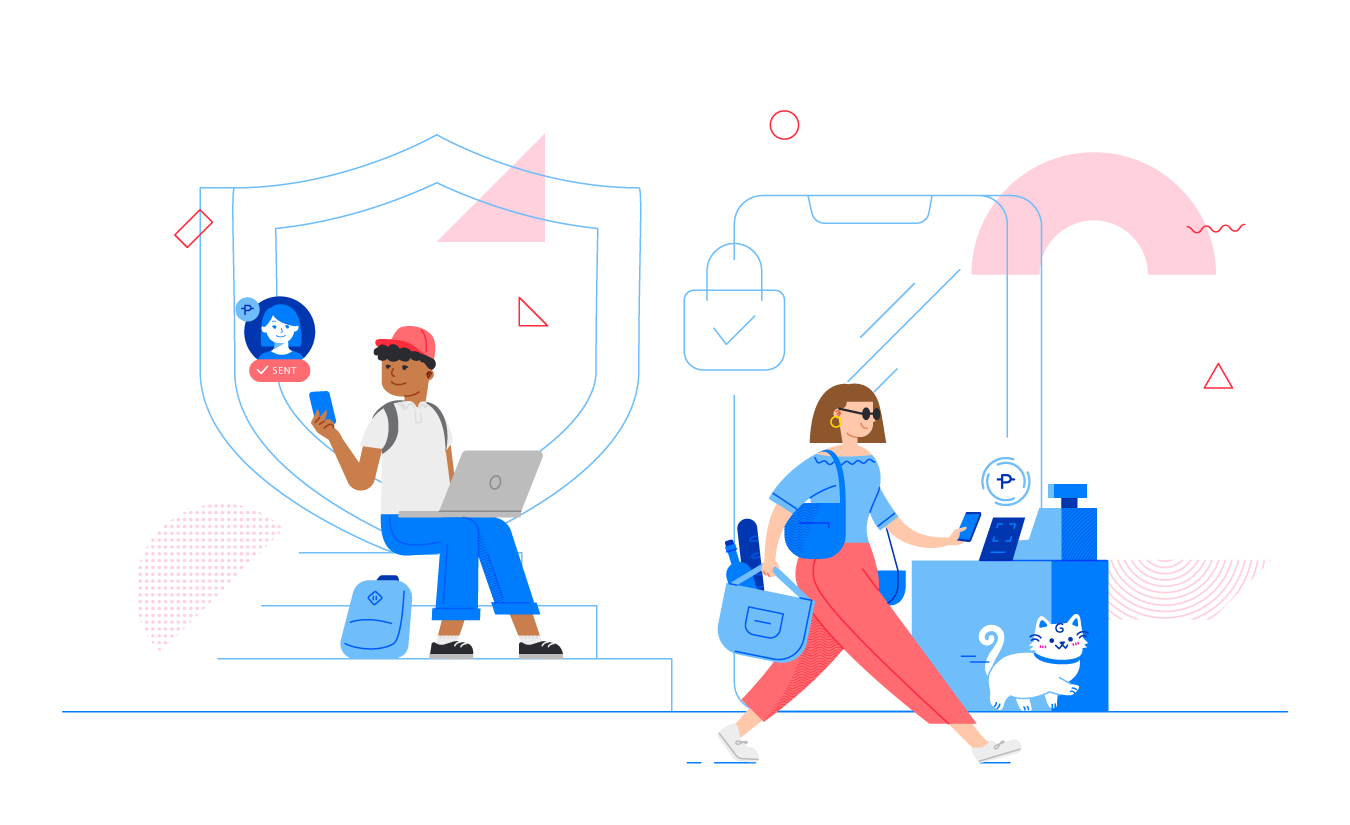

We’ve gone even beyond payments. Own your future and build your success today because with GCash, the Future is Now.

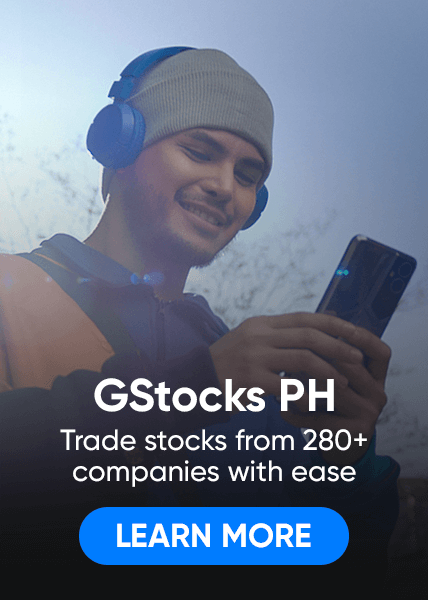

Invest in local stocks, mint the latest NFT collection, pay bills even from abroad, and enjoy cashless travels globally.

THE FUTURE IS NOW

Kaya Mo. I-GCash mo.